Cash Flow, Pricing Power, and the Quiet Return of the Nifty Fifty.

Markets have spent the past decade rewarding spectacle. Growth was defined by disruption, narratives, and distant promises rather than earnings. That regime is fading. In its place, something older and less exciting is reasserting itself. Boring is becoming growth.

Companies that are already profitable, modestly growing, and capable of producing stable cash flows are quietly regaining favor. Firms like Johnson and Johnson, Gilead Sciences, Lululemon, McDonald’s, Saputo, Dollar General, and Airbnb do not depend on heroic assumptions to justify their valuations. They generate real earnings today. Many operate with operating margins in the 20 percent range, return capital consistently, and exhibit pricing power that survives economic slowdowns. This is not stagnation. It is durability.

The numbers explain the shift. With policy rates above 3 percent, risk-free returns are no longer theoretical. Capital now has an alternative. Higher rates mechanically compress the valuation of long-duration assets, particularly thematic and speculative names whose cash flows sit far in the future. As discount rates rise, those valuations become fragile, breaking not on fundamental deterioration, but on absurd or unrelated events. Liquidity no longer forgives.

By contrast, boring companies absorb higher rates far more effectively. McDonald’s generates over 8 billion dollars in annual free cash flow and maintains operating margins above 40 percent through a franchise-heavy model. Lululemon has sustained revenue growth north of 10 percent annually while remaining solidly profitable. Gilead Sciences produces billions in annual cash flow despite minimal headline growth. Dollar General continues to benefit from trade-down behavior, even as consumer sentiment weakens. Airbnb, often misclassified as a growth story, already generates meaningful free cash flow with limited incremental capital requirements.

Beta matters again. Low-beta stocks, long dismissed as defensive relics, now offer something scarce: predictability. In a market overextended for breath and overly focused on thematic revolutions, predictability becomes a competitive advantage. Earnings visibility reduces volatility. Cash flow reduces dependency on capital markets. Pricing power protects margins when inflation reappears where it is least expected.

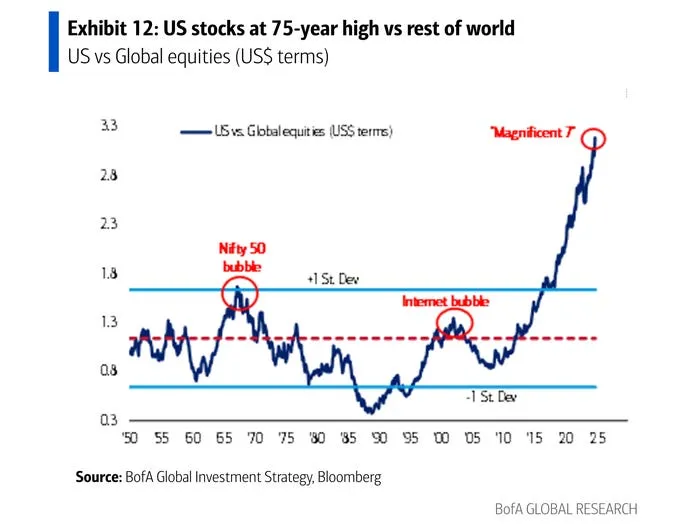

This is how new leadership regimes form. In the late 1960s and early 1970s, the original Nifty Fifty were not exciting companies. They were dominant, profitable, and boring in precisely the right way. Investors paid up for certainty, and for a time, that trade worked extraordinarily well. The lesson was never that valuation does not matter, but that durability commands a premium when uncertainty rises.

The 2020s are unlikely to reward excess imagination the way the 2010s did. Liquidity is scarcer. Rates are higher. Capital is more selective. In that environment, the companies that quietly compound earnings, defend margins, and return cash may once again become the market’s core holdings.

Boring does not mean stagnant. It means survivable. And survivability, once again, is growth.