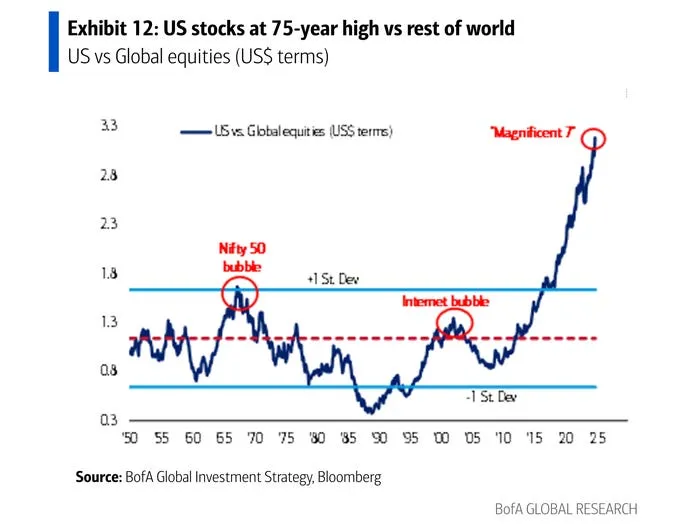

Modern markets like to believe they are safer than the past

Value-at-risk models. Stop losses. Circuit breakers. Stress tests. Scenario trees.

Every institution is armed with a thousand tools designed to manage risk.

And yet drawdowns feel sharper. Liquidity disappears faster. Small shocks metastasize into systemic events.

This is not a contradiction.

It is the consequence.

The uncomfortable truth is this: the dominant source of market risk today is risk management itself.

Snowfalls Don’t Kill Markets. Avalanches Do.

News is a snowfall.

An earnings miss. A CPI print. A geopolitical headline. A policy tweak.

It is rarely fatal on its own.

An avalanche, however, is not caused by the snow.

It is caused by synchronization.

When weight accumulates in the same direction, when stress lines align, when everyone reacts at once, gravity does the rest.

Markets work the same way.

The catalyst is seldom, if ever, large enough to justify the consequence. It simply matters that everyone interprets it the same way at the same time with the same playbook.

Risk Models Don’t Reduce Risk. They Align Behaviour.

In theory, diversification of actors should stabilize markets.

In practice, financial institutions have converged to the same models, metrics, and triggers.

The same volatility thresholds

The same drawdown limits

The same correlation assumptions

The same “de-risk” signals

When one fund cuts exposure, it pushes prices just enough to trip another fund’s risk limits. That selling nudges implied volatility higher, forcing yet another cohort to reduce leverage. Liquidity providers widen spreads or step back entirely. Price becomes signal.

At that point, risk management is no longer defensive-it is offensive.

Liquidity is the first casualty.

Liquidity is not a constant.

It is a function of confidence.

Liquidity feels abundant in tranquil market conditions.

When risk systems trigger, liquidity evaporates precisely when it is needed most.

Herein lies the paradox at the heart of modern finance:

In fact, the very tools designed to protect capital-things like stops and Value at Risk-create liquidity vacuums by forcing identical actions under stress.

What appears as prudence in isolation becomes fragility in aggregate.

The illusion of control.

Risk frameworks are based on one comforting assumption:

that the future will resemble the past closely enough for probability to matter.

But markets do not fail because models are wrong on average.

They fail because they are wrong together.

Extreme events are not statistical outliers.

They are coordination failures.

And coordination failures are endogenous.

Why Volatility Is Not the Enemy

Volatility is often blamed as the villain.

But volatility is just the messenger.

The true peril is compressed volatility–times when risk seems low, positioning gets crowded, leverage grows silently, and everyone thinks exits will stay open.

That is when snow piles up.

When the slope finally gives way, the violence of the move reflects not fear but misplaced confidence.

Survival is asymmetric

The winners in those environments are rarely the fastest traders or the most sophisticated modelers. They are the ones who: Avoid crowded positioning. Tolerate mark-to-market pain Refuse to outsource judgement wholly to models Hold liquidity when it feels unnecessary They know being early will survive; being in sync will not. The Real Risk Question Not the right question is: “What if I am wrong?” It is: “What if everyone were to react the way that I do?” Because in markets shaped by shared risk systems, the marginal seller is not motivated by fear, fundamentals, or even conviction. They are driven by rules. And rules, when followed simultaneously, turn snowfalls into avalanches.