The cruelest lesson in markets is not that you can be wrong. It is that you can be spectacularly right, get the timing wrong by three weeks, and the market will still try to bury you.

The most violent market lesson is not that bubbles exist. Everyone knows bubbles exist. The real lesson is that bubbles can remain solvent longer than your pride, your margin, and your risk manager. That is why the Stanley Druckenmiller internet-short episode still matters. In 1999, while working under George Soros, Druckenmiller put roughly $200 million into short positions against internet stocks after names like Yahoo and AOL had already gone parabolic. By his own telling, the trade turned into a disaster almost instantly: within roughly three weeks, he covered at a $600 million loss. And yet the truly savage part of the story is what came later. He later said he had been short 12 stocks, and every single one of them eventually went bankrupt. In other words, his analysis was not just broadly correct. It was perfect. His timing still nearly killed him.

That is why short selling is one of the most seductive and treacherous activities in finance. On the surface it flatters intelligence. The short seller gets to be the adult in the room, the skeptic, the person who sees through fraud, hype, and multiple expansion dressed up as destiny. But the math is vicious. Druckenmiller himself put it in brutally simple terms: if you are dead wrong on a long, you can lose 100 percent; if you are dead wrong on a short, you can lose ten times your money. That asymmetry is not a detail. It is the whole game. A short is not merely a bet against a stock. It is a bet against market psychology, liquidity, reflexivity, and the capacity of other people to behave like lunatics for longer than you thought possible.

The 1999 dot-com mania was the purest expression of that truth. Even contemporaneous press coverage made clear that Soros funds were badly wounded by internet-stock bets gone wrong during the mania. The trade did not fail because the companies were sound. It failed because the market was in a religious phase, and shorting a religion is dangerous while the congregation is still singing. That is the part retail bears, podcasters, and valuation purists routinely forget. Overvaluation is not a catalyst. Fraud is not a catalyst. Insolvency is not even always a catalyst on your timetable. You can identify the corpse correctly and still get trampled before the funeral begins.

Druckenmiller’s own retrospective makes the point even harsher because he was not some mediocre tourist learning leverage for the first time. This was one of the great macro investors of his generation, a man famous for extraordinary compounding and risk-taking discipline. Yet even he later said he was “not sure” he had ever made money on shorts over a forty-year career. That should be read less as autobiography than as a warning label. If one of the best investors alive can look back on decades of markets and suspect that shorting was a losing game for him overall, then the average modern bear with a brokerage app and a superiority complex should probably assume the odds are not exactly favorable.

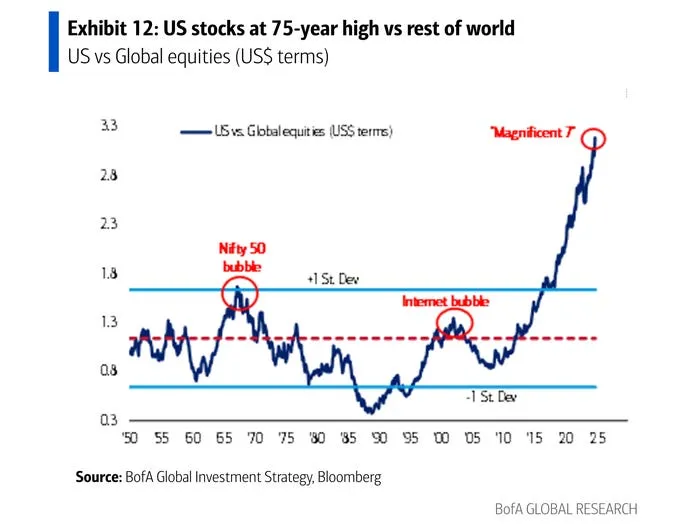

This is what makes the story newly relevant in the AI era. There are obviously stocks today that look absurd. There are companies trading on narrative, on TAM fantasies, on datacenter vapor, on the assumption that every mention of inference demand deserves a trillion-dollar halo. Bears are not crazy to notice this. In many cases they are probably directionally right. Some of today’s AI darlings will indeed disappoint, dilute, implode, or simply deflate into much smaller multiples. But that does not automatically make shorting them intelligent. A crowded long built on mania can levitate on flows, policy enthusiasm, benchmark pressure, and momentum for far longer than any spreadsheet says it should. If Druckenmiller could be perfectly right about 12 doomed internet stocks and still lose $600 million in three weeks, then anyone casually stepping in front of an AI momentum train should at least have the decency to understand what game they are playing.

The deeper truth is that markets do not reward being right in the abstract. They reward surviving the path between mispricing and resolution. That is the entire difference between analysis and P&L. Druckenmiller saw where the story ended, but short sellers do not get paid for writing the last chapter early. They get paid only if they can remain alive, financed, and emotionally intact until the plot finally catches up. Most cannot. That is why so many brilliant shorts become glorious postmortems instead of profitable trades.

So the real moral of Druckenmiller’s dot-com short is not “don’t fight bubbles,” because somebody eventually must. It is something colder: if you short mania, you are not betting against value. You are betting against time, capital structure, and mass delusion all at once. And time is usually the most expensive leg of the trade. Being early is not just similar to being wrong. In leveraged markets, it is often indistinguishable from it.